DeepDive#2 Integra Resources: Producer at a Developer’s Price

Is Integra Too Cheap to Ignore? With one producing mine and two U.S. heap leach projects in development, Integra trades at just 0.22× EV/NPV8%

Summary: Why Integra Resources (ITRG) Is a Producer Trading at a Developer’s Price

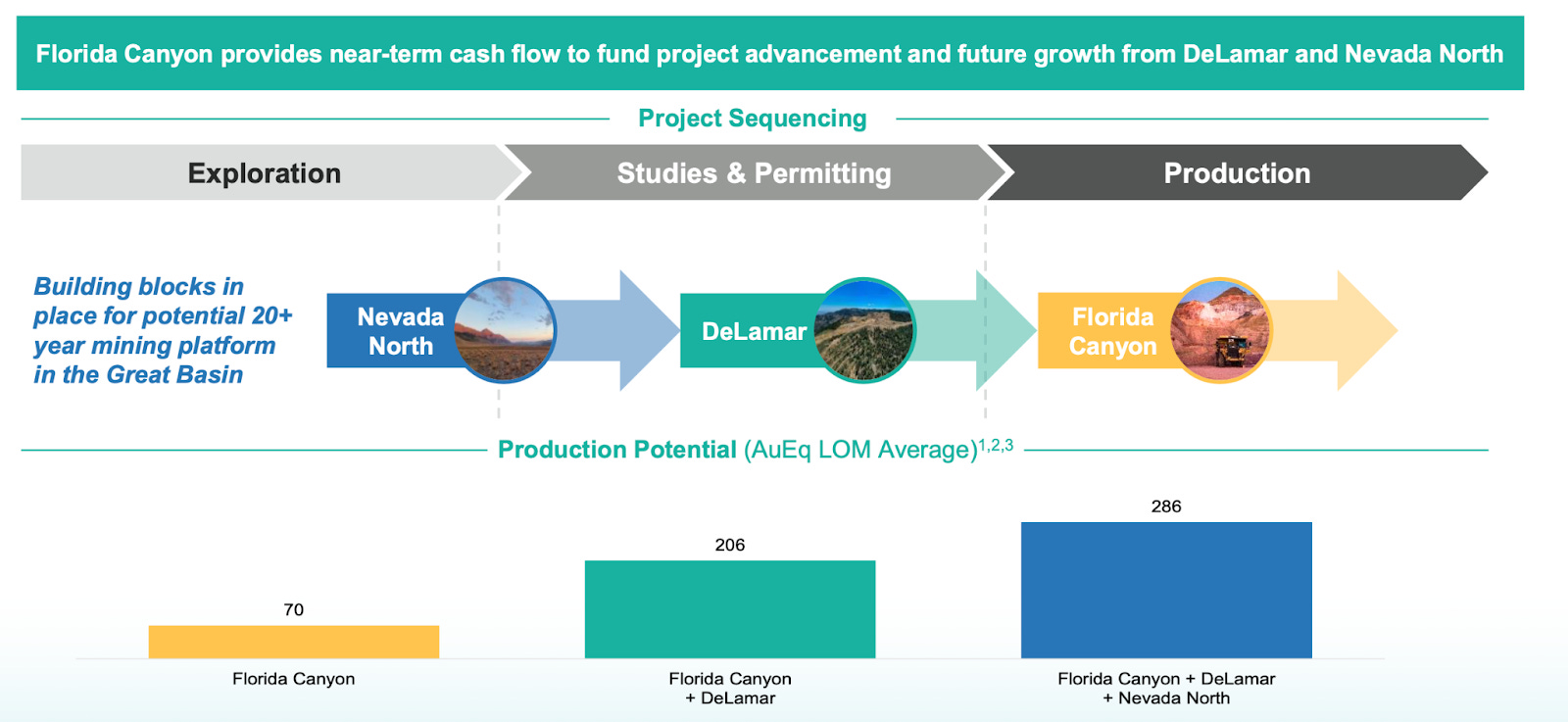

With the acquisition of the Florida Canyon Mine, Integra Resources has transitioned into a U.S. gold producer—generating cash flow that can fund the advancement of its two large-scale heap leach development projects: the flagship DeLamar Project in Idaho and the Nevada North Project in Nevada. This new production base meaningfully reduces dilution risk while unlocking strategic optionality.

Yet the market still values Integra like a pre-production developer. My valuation model suggests the stock trades at just 0.22x EV/NPV8% using $3,000/oz gold—despite a project portfolio that could reasonably support over $1 billion in net asset value.

Upcoming catalysts—including a streamlined Feasibility Study for DeLamar (H2 2025), near-pit drilling aimed at extending Florida Canyon’s mine life (early 2026), and ongoing cash flow generation from Florida Canyon—offer a clear path to closing this discount. The producing asset helps fund development while reducing dilution risk, providing Integra with a stronger financial base than most peers at this stage. However, key risks remain, particularly permitting timelines and an alarmingly low level of insider ownership, which raises concerns about long-term alignment with shareholders.

In this deep dive, I cover:

Florida Canyon’s operational optimization and mine life extension potential

DeLamar’s revised, de-risked development plan

My NPV valuation scenarios across all three key assets

A critical look at management compensation and insider alignment

The 12–24 month roadmap of milestones and risks to monitor

If Integra executes on its next set of milestones—a significant re-rating could follow. Full breakdown below.

Disclaimer Nothing in this post should be taken as financial advice. All opinions and estimates are my own and for informational purposes only. I may hold shares in this company and could be biased. I received no compensation for writing this article. I strive to double-check all data and disclosures, but as a one-person research effort, there may be errors or typos. If you spot anything significant, feel free to reach out. Always do your own research before making investment decisions.

Author’s Note: This deep dive turned out longer than I initially expected—even after cutting some sections. It’s organized by section, so feel free to jump around to the parts you’re most interested in.

Introduction

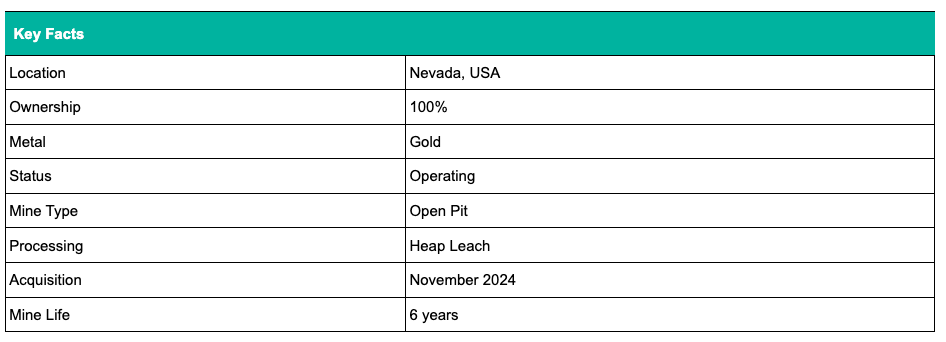

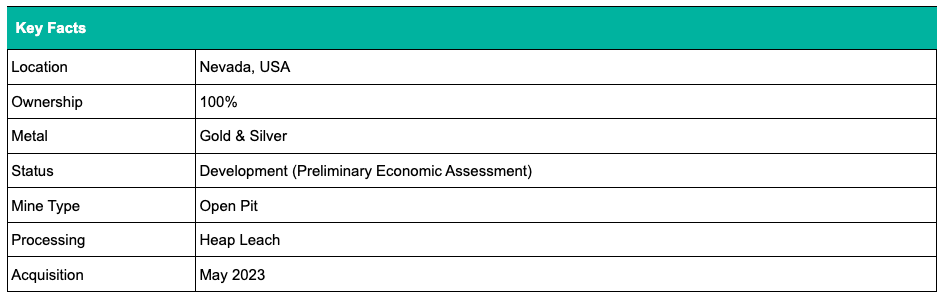

Integra Resources Corp. (TSXV: ITR | NYSE American: ITRG) is a U.S.-focused gold and silver company operating in the Great Basin region of the western United States. In late 2024, the company transitioned from developer to producer with the acquisition of the Florida Canyon Mine in Nevada—a conventional hard rock open-pit operation using both two-stage crushing and run-of-mine (ROM) heap leaching. Originally in continuous production from 1986 to 2011, Florida Canyon was restarted in 2016 and has been operating since. The asset includes a substantial land package of over 18,000 acres, encompassing both the Florida Canyon and the nearby Standard Mine.

Beyond Florida Canyon, Integra is advancing two flagship development-stage assets: the DeLamar Project in Idaho and the Nevada North Project (which includes the Wildcat and Mountain View deposits) in Nevada. Both are envisioned as large-scale open-pit, heap leach operations with meaningful exploration upside.

The company also maintains a portfolio of earlier-stage exploration projects across Idaho, Nevada, and Arizona, including Cerro Colorado, BlackSheep, and War Eagle. Integra’s strategy is to become a mid-tier U.S. gold producer through operational optimization at Florida Canyon and disciplined development of its advanced-stage assets.

Florida Canyon

Florida Canyon is a conventional open-pit operation using both two-stage crushed ore and ROM (run-of-mine) ore placed on heap leach pads. Recovery is achieved through drip irrigation and carbon-in-column (CIC) processing. Final doré production is handled on-site. Recent investments in leach pad expansion (Phase III) and a new CIC circuit commissioned in late 2024 are aimed at improving metal recoveries and inventory turnover. The current life-of-mine plan outlines approximately six years of production, though Integra is actively pursuing several initiatives to extend mine life through resource conversion and near-pit exploration.

Integra acquired the Florida Canyon Mine through the all-share purchase of Florida Canyon Gold Inc. (FCGI), a transaction completed on November 8, 2024. Under the terms of the transaction, Integra issued 0.467 of a common share for each FCGI share outstanding, resulting in the issuance of 65,213,010 Integra common shares to former FCGI shareholders.

Location

Located 125 miles east of Reno, Nevada, and adjacent to Interstate 80 near the town of Imlay, the Florida Canyon Mine is Integra’s sole producing asset and core cash-flow generator. The mine lies in Pershing County within the prolific Humboldt Range and is operated by Integra’s subsidiary, Florida Canyon Mining Inc. (FCMI). The property spans approximately 18,800 acres, combining fee land, patented claims, and 656 unpatented mining claims. Access is year-round, and infrastructure is well developed, including power lines, water rights, and proximity to mining support hubs such as Winnemucca and Lovelock.Reserves

Reserves

As of December 31, 2024, the Florida Canyon Mine hosts Proven and Probable (P&P) reserves totaling 70.4 million tonnes at an average gold grade of 0.35 g/t, containing 785,000 ounces of gold. These reserves are reported at the point of delivery to the process plant and are constrained within open-pit designs optimized at a base case gold price of US$1,800/oz. Cut-off grades range from 0.13 to 0.20 g/t depending on ore type and recovery method, with oxide recoveries varying between 45% and 64%.

Resources

Measured and Indicated (M&I) resources, inclusive of reserves, stand at 77.0 million tonnes grading 0.35 g/t for 854,000 ounces of gold. Inferred resources total 95.8 million tonnes at a higher average grade of 0.72 g/t, equating to 2.22 million ounces. However, the majority of this inferred material is sulfide-hosted and not amenable to Florida Canyon’s current heap leach processing setup. Recovering gold from this material would require construction of a sulfide-capable mill and potentially oxidative treatment, which is not part of the existing mine plan.

The current reserve model also incorporates 1.93 Mt of stockpiled ore at 0.19 g/t and 3.55 Mt of leach pad inventory at 0.29 g/t, collectively containing approximately 44,000 ounces of gold. All estimates were prepared in accordance with CIM Definition Standards and NI 43-101.

Current operation

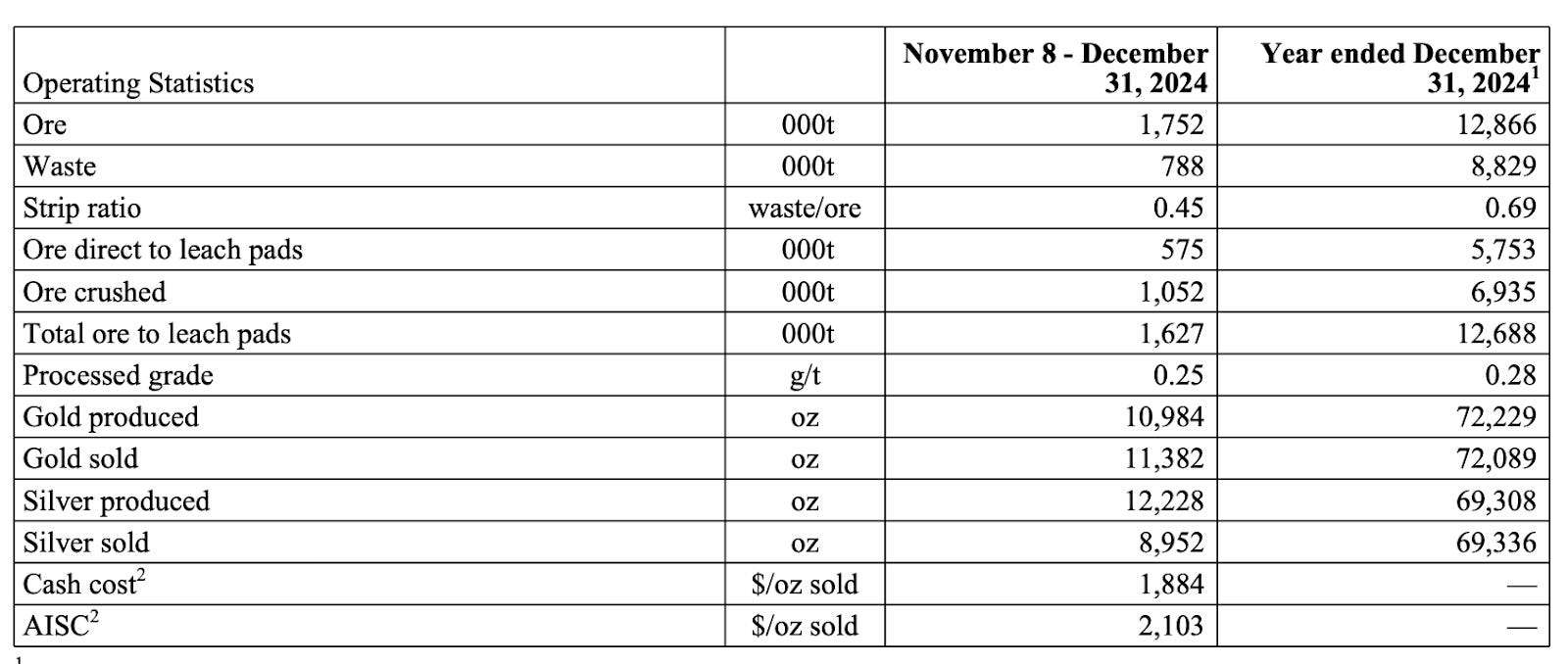

In 2024, the Florida Canyon Mine produced 72,229 ounces of gold and sold 72,089 ounces, including 10,984 ounces of production during Integra’s ownership period beginning November 8, 2024. The average processed grade for the year was 0.28 g/t, with a combined 12.7 million tonnes of ore stacked on the leach pads. During Integra’s period of ownership, the mine reported a cash cost of $1,884/oz and an all-in sustaining cost (AISC) of $2,103/oz.

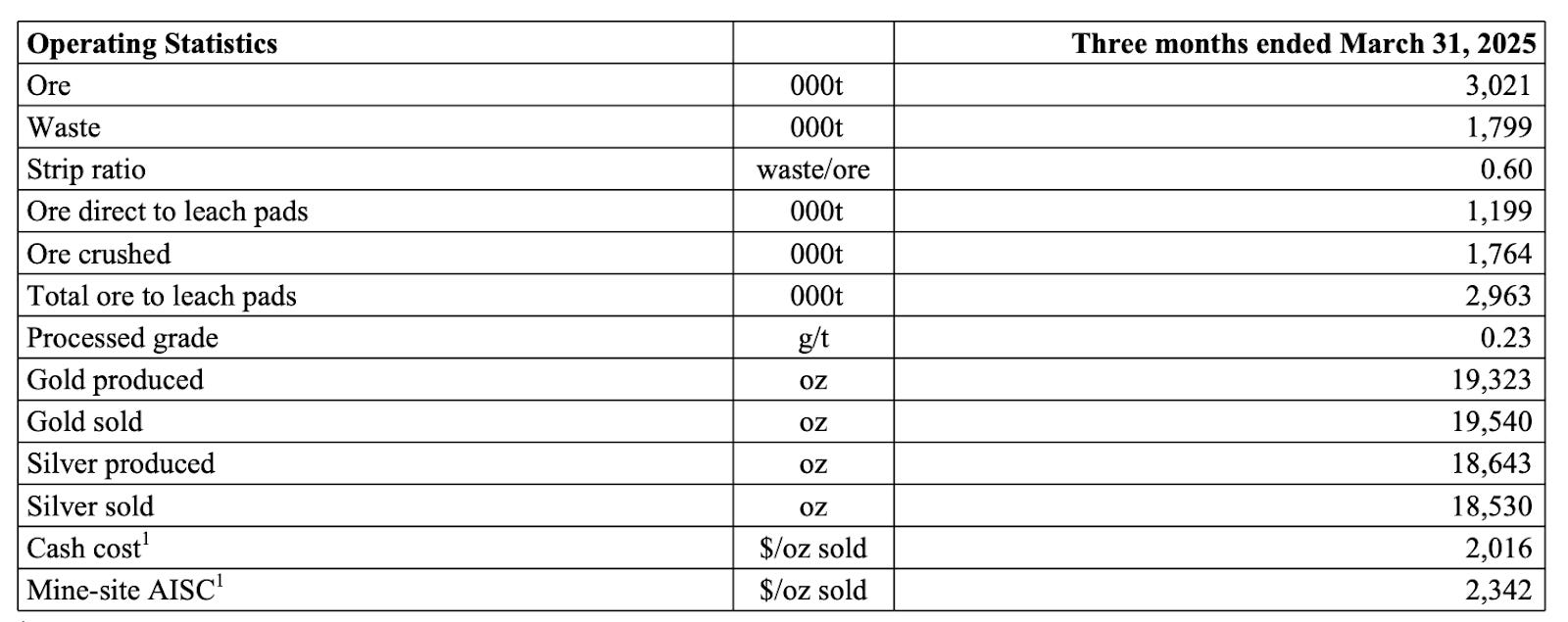

Operations in Q1 2025 continued at a strong pace, with 3.0 million tonnes of ore placed on the pads and a strip ratio of 0.60. Gold production totaled 19,323 ounces, exceeding expectations due to a one-time recovery of ~2,000 ounces of gold from electrowinning tank cleanup—an efficiency project completed early in the year. Additional gains were driven by improved solution flow rates and full commissioning of the new carbon-in-column (CIC) circuit. Gold sales for the quarter reached 19,540 ounces, with cash costs of $2,016/oz and mine-site AISC of $2,342/oz. Total AISC, including corporate-level costs, amounted to $2,446/oz.

Outlook and Near-Term Plans

Integra has outlined several key initiatives at Florida Canyon aimed at optimizing operations and extending mine life. Following the successful commissioning of the new carbon-in-column (CIC) circuit in late 2024, the company continues to ramp up solution flow through the heap leach system to improve recovery rates and reduce leach cycle time. A number of operational optimization studies are underway, including a full review of the mobile equipment fleet—targeting maintenance schedules, replacement cycles, and haulage efficiency. Some of these studies are expected to be completed in the first half of 2025, while others will continue into 2026.

On the capital side, sustaining expenditures for 2025 include a ~$12 million investment in the Phase III-b expansion of the South Heap Leach Pad, which will enhance ore stacking capacity and support continued production into the later years of the current mine plan. In addition, Integra has implemented a gold price protection program for 2025 by purchasing put options, securing downside protection while retaining full upside exposure.

Exploration efforts are also underway to support resource conversion and mine life extension. A 10,000-meter reverse circulation (RC) drilling campaign was launched in May 2025, focused on near-mine oxide targets within the current pit shells. With a budget of $1.5 million, this program aims to define additional reserves and upgrade inferred resources. Initial drill results are expected in the summer, and a revised mineral resource and life-of-mine plan is anticipated in early 2026.

Author Commentary

From an investor perspective, I believe Florida Canyon offers meaningful potential for operational improvement and mine life extension beyond the current six-year plan. Management commentary has been notably optimistic, suggesting that ongoing drilling and optimization work could support an additional 2–4 years of production. This would significantly enhance the asset’s value, especially given the infrastructure and processing capacity already in place.

Integra expects to release formal 2025 production and cost guidance in Q2, which should provide further clarity on the trajectory for this year. As I’ll outline in the valuation section, I model a base case aligned with the current LOM plan but also incorporate an extension scenario to reflect the upside potential being pursued.

DeLamar

The DeLamar Project is Integra’s flagship development-stage asset, located in southwest Idaho’s Owyhee County—a region with a long mining history. The project encompasses the past-producing DeLamar and Florida Mountain deposits, which were historically operated by Kinross Gold until their closure in the late 1990s. Integra acquired 100% of the asset in 2017 and has since made progress in expanding the resource base and advancing toward production.

DeLamar is envisioned as a large-scale, open-pit heap leach operation targeting gold and silver extraction. The company completed a Preliminary Economic Assessment (PEA) in 2019 and followed up with a more detailed Pre-Feasibility Study (PFS) in 2022. Most recently, Integra published an updated Mineral Resource Estimate in 2023, which for the first time included legacy stockpiles and backfill material left by previous operators. The project is currently in the permitting phase with the U.S. Bureau of Land Management (BLM), with active stakeholder engagement and baseline environmental studies underway.

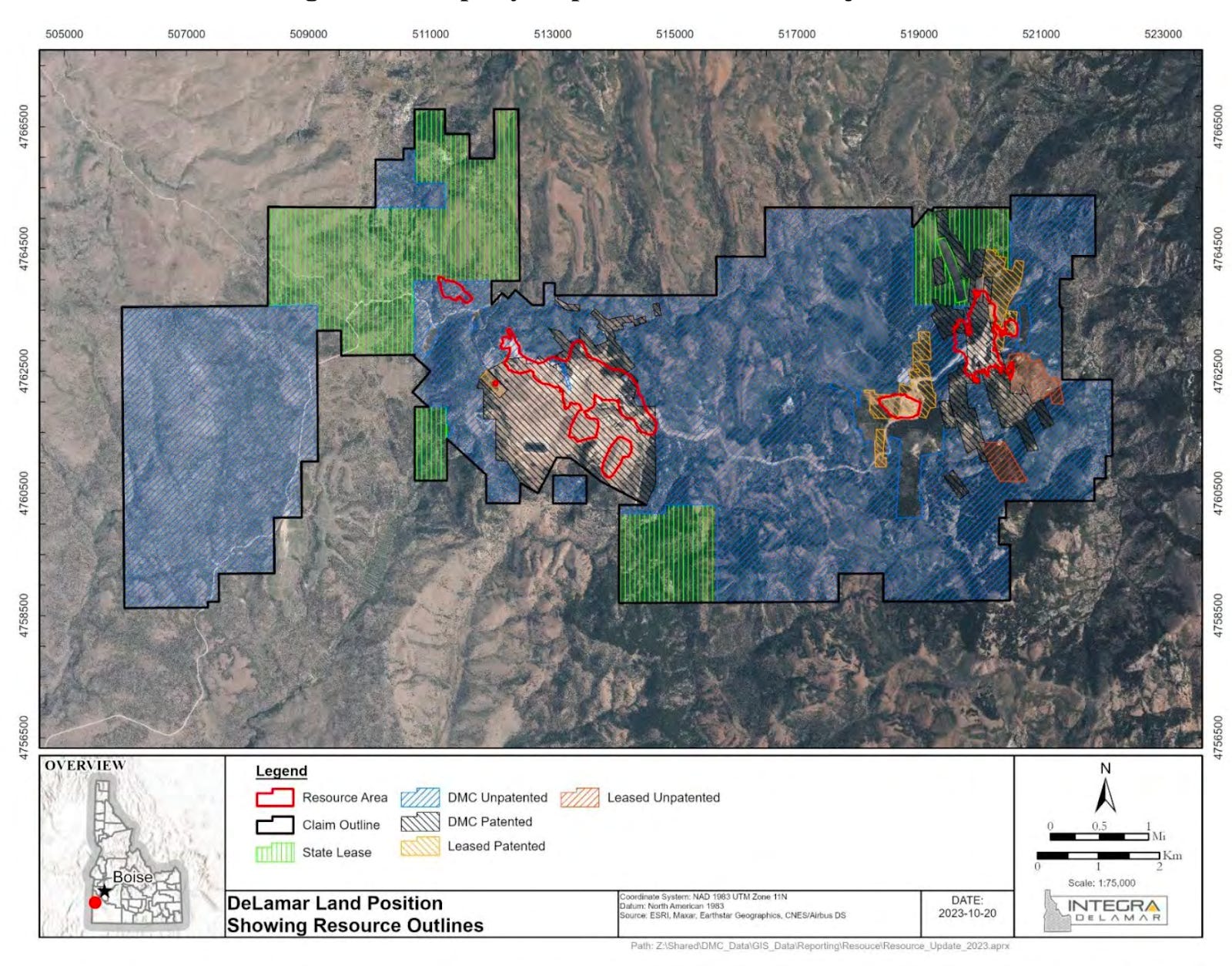

Reserves

As of January 24, 2022, the DeLamar Project hosts Proven and Probable (P&P) reserves totaling 123.5 million tonnes grading 0.45 g/t gold and 23.27 g/t silver, containing 1.79 million ounces of gold and 92.4 million ounces of silver. These reserves span both the DeLamar and Florida Mountain deposits and are defined at the point of crusher feed. Reserve modeling was based on optimized open-pit designs using gold and silver prices of US$1,650/oz and US$21.00/oz, respectively, with cut-off grades tailored to material type and processing route:

Florida Mountain oxide (heap leach): US$3.55/t

DeLamar oxide (heap leach): US$3.65/t

Non-oxide (mill): US$10.35/t to US$15.00/t

The reserve plan supports initial heap leach production followed by mill construction in year 3 to process non-oxide ore.

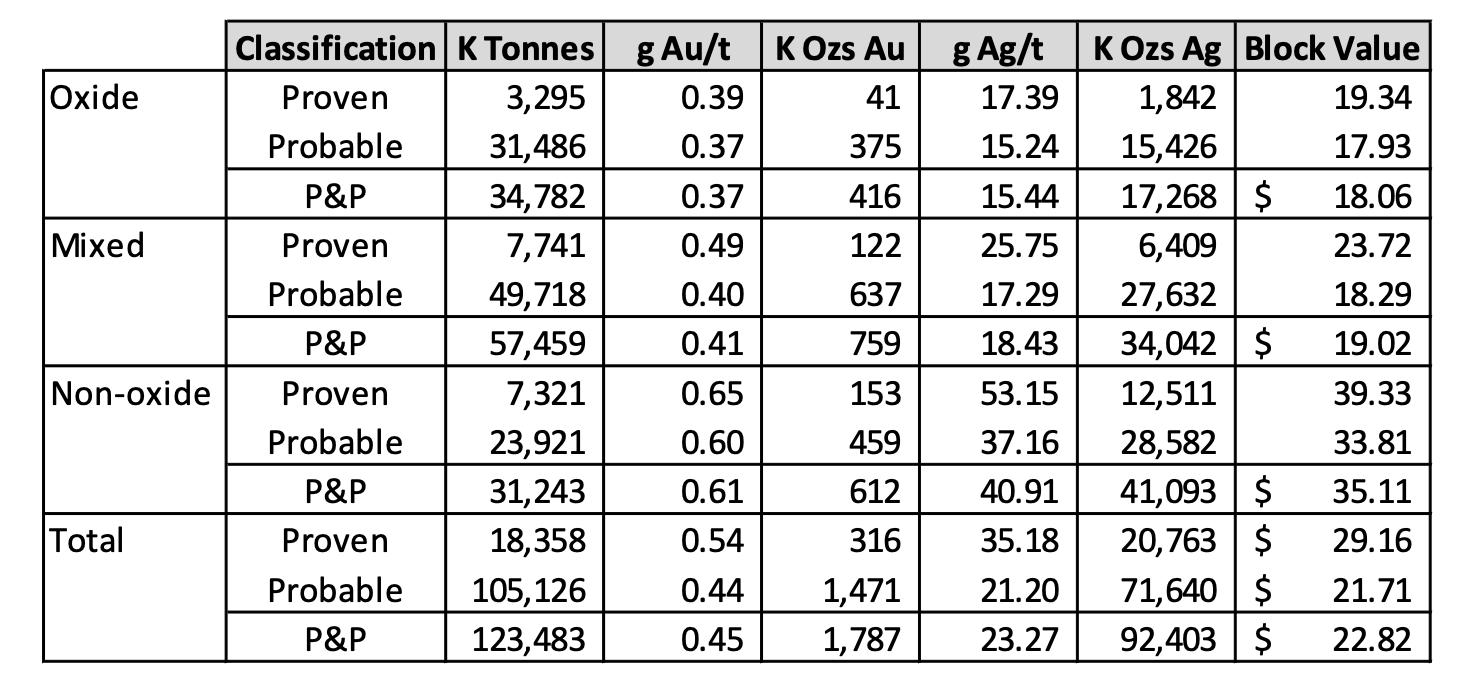

Resources

The updated mineral resource estimate, effective August 25, 2023, expands the project’s inventory by incorporating additional in-situ mineralization and legacy stockpiles. Total Measured and Indicated (M&I) resources, inclusive of reserves, now stand at 247.8 million tonnes grading 0.37 g/t gold and 18.1 g/t silver, containing 2.94 million ounces of gold and 142.7 million ounces of silver. Inferred resources add a further 43.1 million tonnes at 0.31 g/t gold and 10.8 g/t silver (428,000 oz Au and 15.0 Moz Ag).

Resources were constrained within Whittle-optimized pits and reported using gold-equivalent (AuEq) cutoffs reflecting different metallurgical pathways:

Oxide & mixed (heap leach): 0.10–0.17 g/t AuEq

Stockpiles: 0.10 g/t AuEq

Non-oxide (mill): 0.20 g/t at Florida Mountain and 0.30 g/t at DeLamar

The resource model reflects a blend of open-pit extractable oxide, mixed, and sulfide mineralization. Heap leaching is the primary method for early-year production, with sulfide ores requiring flotation and agitated leaching in a dedicated processing plant. Notably, no agglomeration is required at Florida Mountain, while approximately 45% of DeLamar’s heap-leach ore will require agglomeration due to its finer grain size and clay content.

All resource and reserve estimates were prepared in accordance with NI 43-101 and CIM Definition Standards.

2022 Preliminary Feasibility Study Summary

Based on: “Technical Report and Preliminary Feasibility Study for the DeLamar and Florida Mountain Gold-Silver Project, Owyhee County, Idaho, USA,” prepared by RESPEC and others, effective date January 24, 2022; reproduced in the updated NI 43-101 technical report dated August 25, 2023.

Mining Method:

The PFS envisions conventional open-pit mining of both deposits, with ore transported via a Railveyor light-rail haulage system to a centralized crushing facility. The system is designed to reduce diesel consumption and support Integra’s decarbonization goals. Waste will be backfilled or deposited in nearby storage facilities, with some used in tailings dam construction.

Owner-operated fleet with 136-tonne trucks and hydraulic shovels.

Strip ratio optimized through phased pit designs.

Ore stockpiling and selective ore routing support throughput flexibility.

Processing:

Two distinct flowsheets are used depending on ore type:

Oxide and mixed material will be heap leached after three-stage crushing to P80 of 12.7 mm. Material from DeLamar may require agglomeration.

Non-oxide material (starting in Year 3) will be processed via milling, flotation, regrind, and agitated cyanide leaching of concentrate.

All pregnant solutions—heap leach and mill—report to a shared Merrill-Crowe plant, producing gold-silver doré.

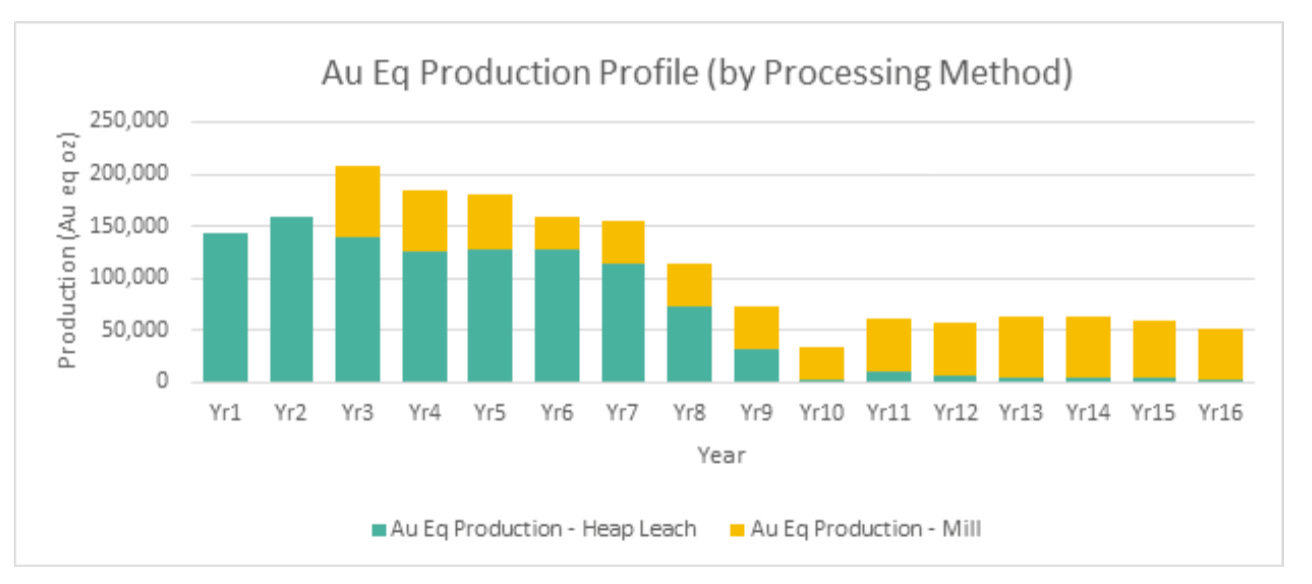

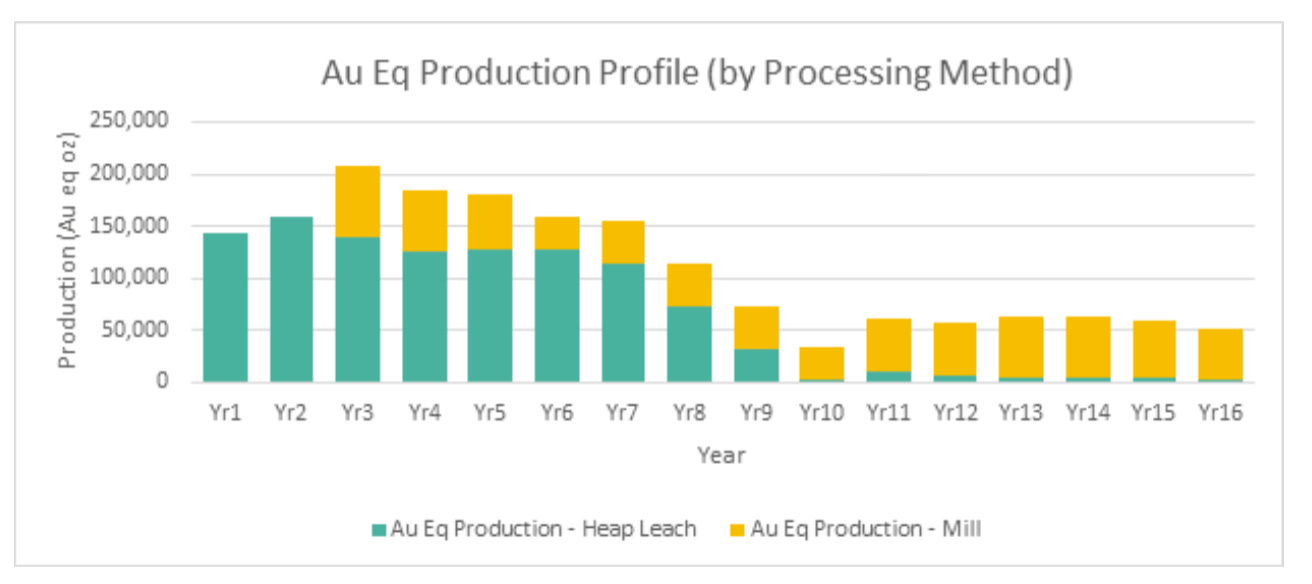

Production Profile:

Average production Years 1–8: 163,000 oz AuEq/year (121,000 oz Au + 3.3 Moz Ag)

Life-of-Mine (16 years): 110,000 oz AuEq/year (71,000 oz Au + 3.1 Moz Ag)

Total recovered gold: 1.15 Moz, silver: 50 Moz

Metallurgical Recoveries:

Heap leach: 72% gold, 37% silver average recovery

Mill (non-oxide): 51% gold, 75% silver average recovery

No agglomeration required at Florida Mountain; ~45% of DeLamar ore will need it.

Capital Costs Summary

Initial capital: US$307.6 million, covering heap leach construction, oxide plant, infrastructure, and working capital.

Sustaining and expansion capital: US$281.8 million, including build-out of the non-oxide mill and tailings facilities.

Total LOM capital: US$589.5 million, inclusive of reclamation and contingency.

Operating Costs:

Mining cost: $1.90/t mined

LOM Processing cost: $12.93/t processed

Cash Cost: $923/oz AuEq

Site-Level AISC: $955/oz AuEq

Economics (Base Case at $1,700/oz Au, $21.50/oz Ag):

NPV5% (after-tax): $407.8 million

IRR (after-tax): 27%

Payback: 3.34 years

Cumulative LOM Free Cash Flow: $689 million

Latest Developments & Outlook

Integra’s objective is to advance and de-risk the DeLamar Project, leveraging a favorable regulatory backdrop in the U.S. to accelerate development. The company is prioritizing a streamlined, environmentally enhanced mine plan while laying the groundwork for future project expansion.

Permitting Milestones

Mine Plan of Operations (MPO): In March 2025, Integra submitted its revised MPO to the U.S. Bureau of Land Management (BLM). The new plan features a more compact project footprint and incorporates design changes aimed at reducing carbon emissions and water usage.

NEPA Process: The MPO submission initiates the National Environmental Policy Act (NEPA) process, starting with a Notice of Intent (NOI). The permitting process will involve environmental scoping, stakeholder engagement, and the development of a full Environmental Impact Statement (EIS). This review is expected to take approximately two years, with Integra targeting progression to the NOI stage before year-end 2025.

Feasibility Study (H2 2025)

A new Feasibility Study (FS) is currently underway, with results expected in the second half of 2025. Forte Dynamics was contracted in 2024 to oversee metallurgical and infrastructure testing, including bottle rolls, column leach tests, permeability studies, and geotechnical investigations.

Notably, the updated FS will focus solely on an oxide-only, heap-leach operation. This represents a shift from the 2022 PFS, which included both heap leaching and sulfide milling. The simplified scope is intended to accelerate permitting and lower upfront capital intensity.

Strategic Shift: Oxide-Only First, Sulfide Later

The decision to exclude non-oxide processing from the initial FS reflects a phased development strategy. While the 2022 PFS confirmed technical viability of milling and agitated leach recovery for sulfide material, Integra is deferring this stage to reduce initial complexity and permitting risk.

Future development of sulfide processing infrastructure remains a longer-term option and could be reintroduced if economics and market conditions warrant.

Exploration & Resource Advancement

The 2023 resource update was the first to include legacy stockpile material, expanding the oxide inventory and supporting the revised heap-leach strategy. Additional drilling, metallurgical testwork, and engineering are planned to further support future reserve conversion and mine life extension.

Nevada North: Wildcat & Mountain View

Integra’s Nevada North Project comprises two advanced-stage oxide gold deposits—Wildcat and Mountain View—located in Pershing and Washoe Counties, Nevada. These assets were acquired through Integra’s 2023 at-market merger with Millennial Precious Metals, which closed in May 2023. The transaction was a strategic step that expanded Integra’s footprint in Nevada and added significant oxide-hosted gold resources in a premier jurisdiction.

Both deposits had seen historical exploration but were largely underdeveloped prior to consolidation by Millennial. Since the acquisition, Integra has advanced the projects through systematic technical work and drilling. A maiden Preliminary Economic Assessment (PEA), filed in mid-2023, outlines a combined development scenario in which the Wildcat and Mountain View deposits are mined sequentially and processed via heap leaching.

The two deposits are located roughly 65 km apart and are accessible by paved and dirt roads from Reno. Integra envisions Nevada North as a low-cost, scalable project with district-scale exploration upside and potential operational synergies with the nearby Florida Canyon Mine.

Resources

As of June 28, 2023, the Nevada North Project (comprising the Wildcat and Mountain View deposits) hosts a combined mineral resource estimate prepared in accordance with NI 43-101 and CIM Definition Standards. All resources are classified as Indicated or Inferred and are reported at a 0.15 g/t gold cut-off, assuming open-pit mining and heap leaching.

Indicated Resources: 88.6 Mt at 0.46 g/t Au and 3.45 g/t Ag, containing 1.32 Moz gold and 9.84 Moz silver

Inferred Resources: 26.6 Mt at 0.32 g/t Au and 2.60 g/t Ag, containing 271 koz gold and 2.22 Moz silver

The Wildcat estimate is based on US$1,800/oz gold, US$2.40/t mining, and US$3.70/t processing costs, with gold recoveries ranging from 52% to 73%. At Mountain View, similar economic assumptions were applied, with recoveries ranging from 30% to 86% and a lower processing cost of US$3.10/t. Silver recoveries average 18–20% across both deposits.

2023 Preliminary Economic Assessment (PEA)

The PEA, dated July 2023, evaluated the combined development potential of Wildcat and Mountain View as a phased, heap-leach gold operation. Key economic highlights at base case prices ($1,700/oz Au, $21.50/oz Ag):

After-tax NPV5%: US$309.6 million

IRR (after-tax): 36.9%

Payable AuEq over LOM: 1.04 Moz

LOM average annual production: 80,000 oz AuEq (Years 1–5: ~94,000 oz AuEq/year)

AISC: US$973/oz AuEq

Initial Capex: US$115 million (to commence at Wildcat)

The operation is planned as an open-pit, heap leach project focused on low strip ratios (1.21 LOM, and just 0.28 at Wildcat), supporting a robust cash cost profile. Combined net free cash flow over the life of mine is projected at US$485 million.

Metallurgy & Recovery

Wildcat: Average heap leach recovery of 71.4% Au (oxide + transitional)

Mountain View: Higher average recovery of 77.1% Au

Silver recoveries are poor across both deposits (18–20%)

The process flow envisions conventional three-stage crushing followed by cyanide heap leaching, aligning with Nevada’s established oxide gold mining framework.

Permitting & Next Steps

Integra is working to streamline the Nevada permitting path:

Wildcat Exploration EA: Completed in 2024; pending Finding of No Significant Impact (FONSI) and Decision Record, expected mid-2025

Upcoming Programs: Metallurgical testing (H2 2025), geochemistry studies (Q2 2025)

Permit Strategy: Accelerate timeline and reduce risk exposure by integrating phased approvals and early-stage data package.

Exploration Assets

In addition to its three core projects, Integra holds a diverse portfolio of early-stage exploration properties across the western U.S., focused primarily on epithermal and Carlin-style gold systems.

BlackSheep District (Idaho)

Located 6 km northwest of DeLamar, BlackSheep hosts multiple epithermal centers with minimal historic drilling. Mapping by experts including Drs. Hedenquist and Sillitoe suggests a preserved high-grade system ~200 m below surface. The district is geologically comparable in scale to DeLamar and Florida Mountain combined.

War Eagle (Idaho)

Situated 3 km east of Florida Mountain, War Eagle is a past-producing gold-silver system acquired via option agreement. It shares similar mineralization styles with Florida Mountain and remains a prospective satellite target.

Nevada Portfolio

Integra’s Nevada land package spans several underexplored targets:

Red Canyon (Eureka District): 6,650 acres with 10 drill-ready Carlin-type gold targets.

Ocelot (Shoshone Mountains): 3,515 acres with low-sulfidation epithermal potential; strong alteration and pathfinder geochemistry.

Marr (Antelope Valley): 1,921 acres showing epithermal indicators beneath cover.

Eden & Dune (Sleeper-Sandman Trend): Low-sulfidation epithermal systems with geologic similarities to known producers.

Cerro Colorado (Arizona): 10,097-acre silver-gold and porphyry copper target in a historic district southwest of Tucson. In June 2024, Integra signed an option agreement with Green Light Metals to potentially divest this asset.

While still early stage, these properties offer optionality and future growth potential, especially BlackSheep, which could evolve into a satellite resource to DeLamar with further drilling.

Wheaton Precious Metals Partnership

Integra Resources has established a relationship with Wheaton Precious Metals (WPM), one of the largest precious metals streaming and royalty companies globally. This relationship spans both equity financing and royalty agreements:

2023 Equity Placement (Millennial Transaction):

As part of the Millennial acquisition, Wheaton invested C$10.5 million through a non-brokered private placement, purchasing 6 million subscription receipts at C$1.75/share.Right of First Refusal (ROFR):

As part of the 2023 equity deal, Integra granted WPM a right of first refusal on any future precious metal streams, royalties, or prepay transactions involving current and future Integra projects—extending 5 km around the acquired Millennial land package and any future associated properties. This restricts Integra from engaging with third-party streamers without first offering terms to Wheaton.2024 DeLamar NSR Deal:

In February 2024, Wheaton acquired a 1.5% Net Smelter Return (NSR) royalty over all claims at the DeLamar Project for a total of US$9.75 million, paid in two equal installments in Q1 and Q3 2024. The transaction further cemented Wheaton’s strategic commitment and provided Integra with non-dilutive funding ahead of its updated Feasibility Study.

Wheaton currently owns approximately 4.2% of Integra’s outstanding shares. Its equity position and royalty investment suggest confidence in the long-term potential of the DeLamar Project.

Management and Board of Directors

Integra Resources is led by a team with demonstrated expertise in open-pit and heap-leach mining, U.S. permitting, and project development across multiple jurisdictions. This aligns directly with its pipeline—optimizing Florida Canyon, advancing DeLamar permitting, and progressing Nevada North.

Recent Executive Changes

January 2025: George Salamis appointed President & CEO; Anna Ladd‑Kruger became Board Chair; Jason Kosec stepped down.

February 2025: Dale Kerner joined as Vice President, Permitting.

March 2025: Clifford Lafleur became Chief Operating Officer.

Key Individuals & Relevant Experience

George Salamis – President, CEO & Director

• Over 30 years in exploration, M&A, and corporate development

• Led Integra Gold to a C$590M acquisition by Eldorado Gold

• Former roles at Placer Dome and Cameco

Anna Ladd‑Kruger – Chair of the Board

• CPA with 25+ years in mining finance

• Former CFO at McEwen Mining; North American Group Controller at Kinross Gold

• Experience spans exploration, permitting, and operations across multiple jurisdictions

Clifford Lafleur – Chief Operating Officer

• Appointed March 2025 to lead Florida Canyon operations and cost optimization

• Former SVP Operations at SilverCrest Metals (Las Chispas Mine)

• Leadership roles at Torex Gold in mine planning, reserve estimation, and open-pit/underground development

Dale Kerner – Vice President, Permitting

• Joined February 2025 with 25+ years of U.S. environmental permitting experience

• Oversaw NEPA approval for Perpetua’s Stibnite Gold Project in Idaho

Timo Jauristo – Independent Director

• 35+ years in mining, including senior roles at Goldcorp and Placer Dome

• Specialist in global project evaluations, M&A, and development strategy

C.L. “Butch” Otter – Independent Director

• Former Idaho Governor (2007–2019), Lieutenant Governor, and U.S. Congressman

• Deep knowledge of Idaho’s political and regulatory environment

Carolyn Clark Loder – Independent Director

• 30+ years in U.S. mineral rights, land management, and tribal relations

• Held senior positions at Freeport-McMoRan and LafargeHolcim

• Served on multiple BLM advisory councils

Eric Tremblay – Independent Director

• 30+ years in mine construction and operations

• Former GM at Canadian Malartic and IAMGOLD’s Westwood Project

• Currently COO at Dalradian Resources

Ian Atkinson – Independent Director

• Former CEO of Centerra Gold

• Senior roles at Kinross, Hecla, Noranda

• Expertise in exploration, resource development, and M&A

Janet Yang – Independent Director

• Over 20 years in capital markets, corporate strategy, and financial leadership

• CFO at Reveam Inc.; formerly CFO of W&T Offshore

• Led US$1.7B in financing transactions

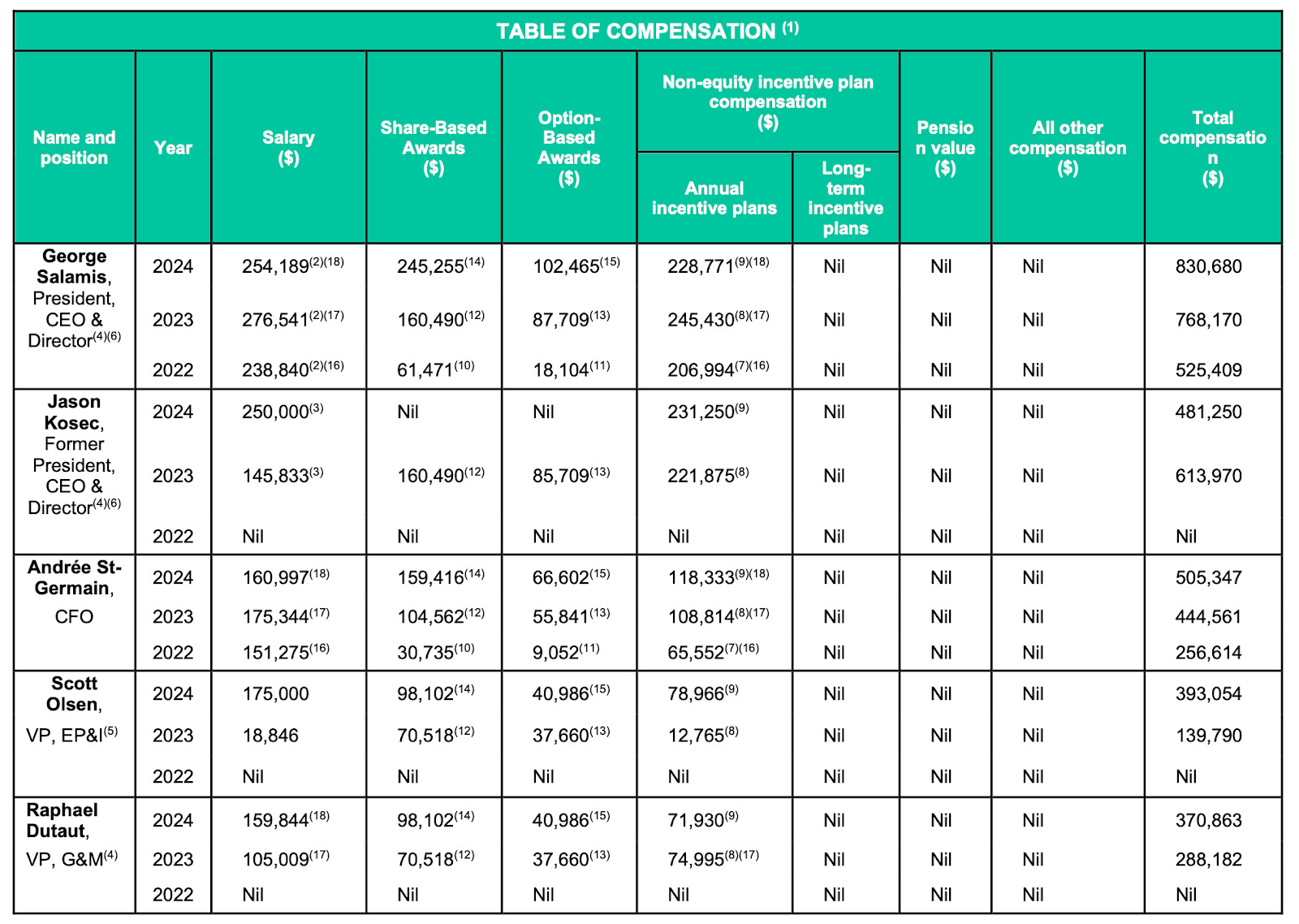

Management Compensation

George Salamis (President & CEO) received total compensation of US$830,680 in 2024, consisting of:

US$254,189 base salary

US$245,255 in share-based awards

US$102,465 in option-based awards

US$228,771 in annual performance-based incentives

Jason Kosec (Former CEO) received US$481,250 in 2024, reflecting his transitional role prior to stepping down in early 2025.

Andrée St-Germain (CFO) earned US$505,347, with nearly half of that tied to equity-based compensation, and approximately US$118,000 from performance incentives.

Overall, base salaries are reasonable, and a substantial portion of total pay is tied to performance and equity.

Performance criteria

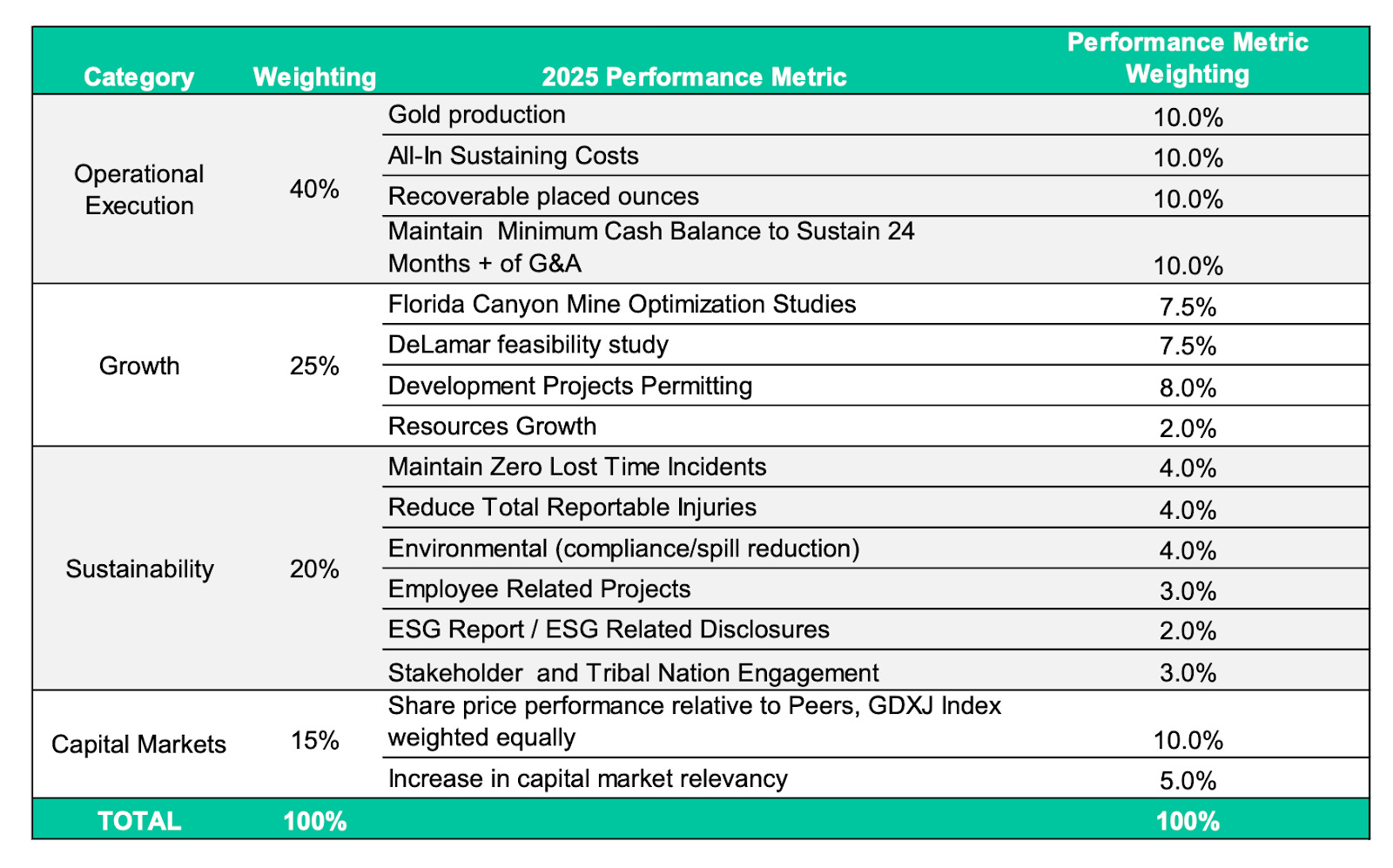

Integra Resources’ executive compensation includes both short-term and long-term incentive components:

Short-Term Incentives (STI):

Executives are eligible for annual cash bonuses of up to 50–100% of base salary, depending on role. Bonuses are based on the achievement of both corporate objectives (75%) and individual objectives (25%). In 2024, the board determined that 90% of corporate goals were met, and bonuses were paid accordingly in early 2025.Corporate objectives include operational metrics (production, AISC, recoverable ounces), permitting progress, feasibility milestones, ESG performance, and capital markets outcomes.

For 2025, objectives have been updated to reflect Integra’s transition to a producing company.

Long-Term Incentives (LTI):

Executives receive annual grants of stock options and RSUs, which vest over three years (1/3 per year). Awards are performance-based.

Overall, I view the incentive design as well structured, with meaningful weight on operational delivery and value creation. The STI/LTI balance supports both annual performance and long-term focus.

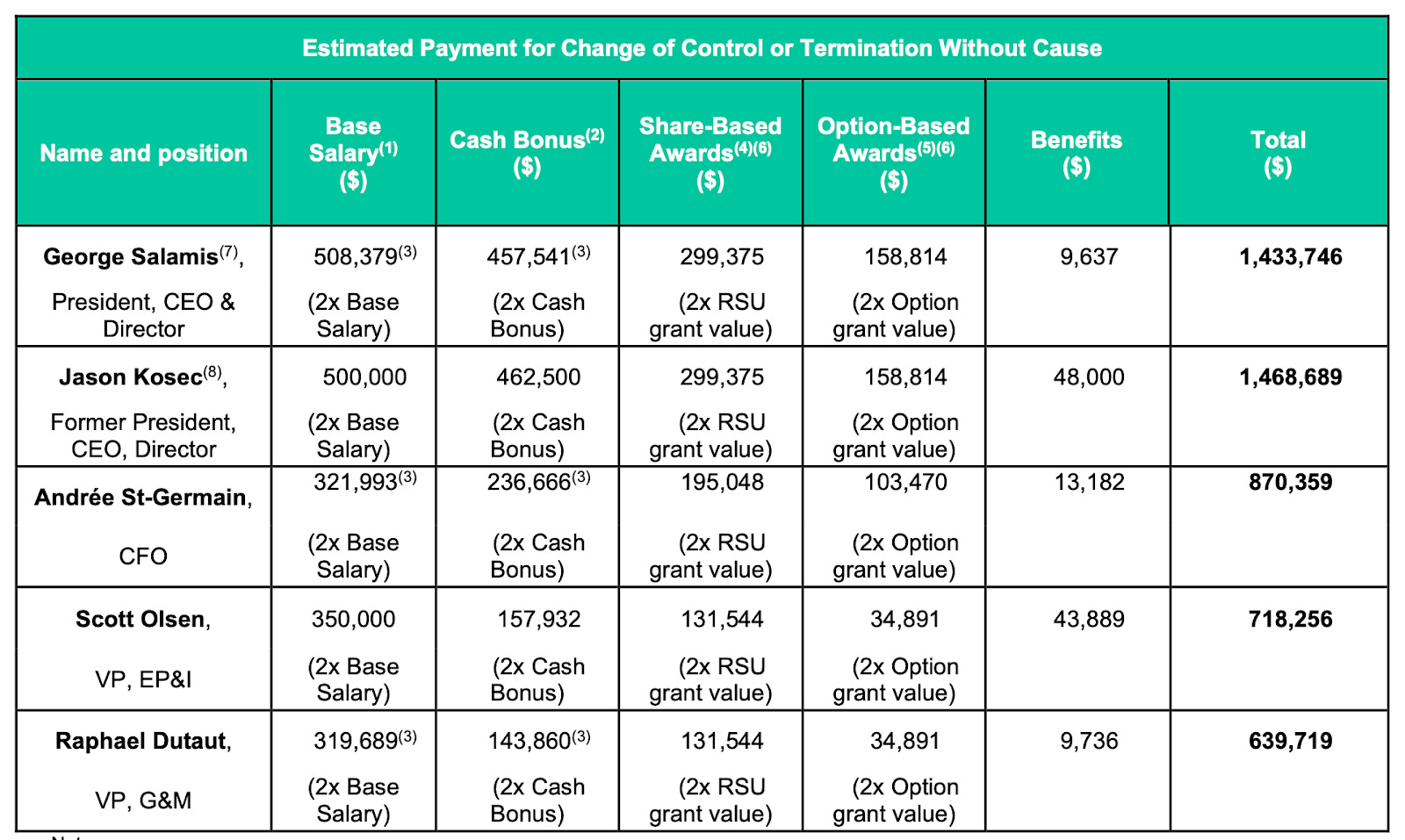

Change of Control and Termination Benefits

As of December 31, 2024, termination without cause or a change of control fees are as follows: 2× base salary, 2× target bonus, and accelerated vesting of equity awards (RSUs and options).

Estimated payouts for key executives :

George Salamis (CEO): US$1.43 million

Jason Kosec (Former CEO): US$1.47 million

Andrée St-Germain (CFO): US$870,000

Scott Olsen (VP, EP&I): US$718,000

Raphael Dutaut (VP, G&M): US$640,000

These figures include salary, bonus, accelerated equity, and benefits. Equity values are based on 2× the 2024 grant value, with full vesting triggered upon a change of control.

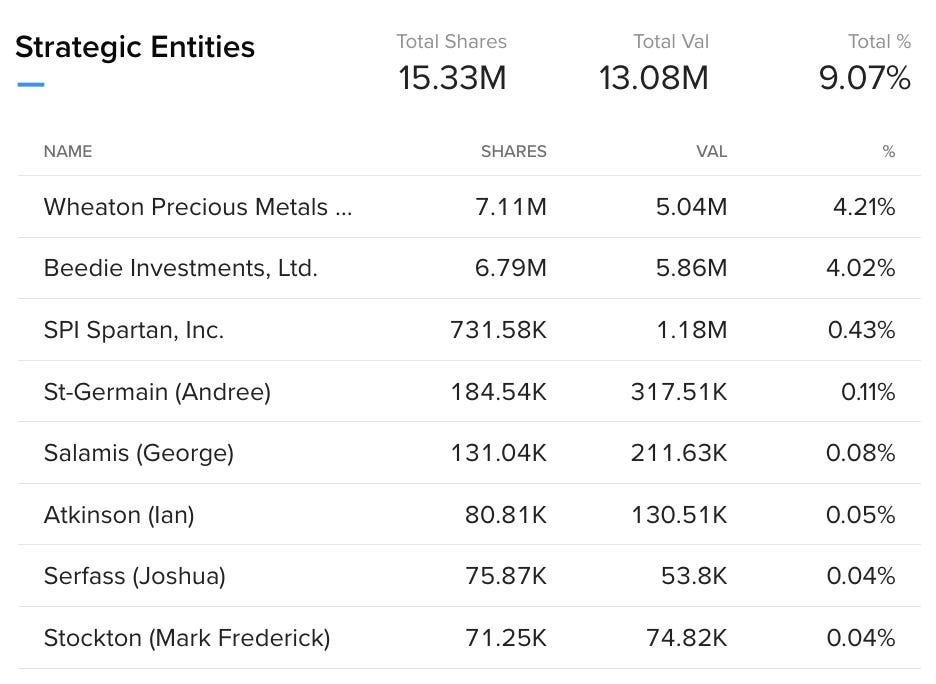

Insider Ownership

As of June 2025, insider ownership at Integra Resources is very limited. Only CEO George Salamis holds a meaningful equity position relative to compensation levels. While he owns approximately 862,620 common shares, either directly or indirectly (via SPI Spartan), this is around two year’s worth of total CEO compensation—but still below the level I’d prefer to see, ideally closer to 5× annual salary.

Other executives and directors hold only modest equity stakes, often limited to Deferred Share Units (DSUs), options, or Restricted Share Units (RSUs). For example:

Anna Ladd-Kruger, Chair of the Board, owns just 4,800 common shares, with most of her exposure through DSUs and options.

COO Clifford Lafleur and VP Permitting Dale Kerner, both recently appointed, currently hold no common shares.

Most independent directors—including Timo Jauristo, Eric Tremblay, and Ian Atkinson—have no or very limited direct ownership in common shares.

Overall, I view this low level of insider ownership as a big negative, as it reflects limited alignment with long-term shareholders. That said, given several recent management appointments, I’ll be watching closely to see if they begin accumulating stock in the open market.

Share Structure

Share Structure Summary (as of March 31, 2025)

Basic shares outstanding: 168.7 million

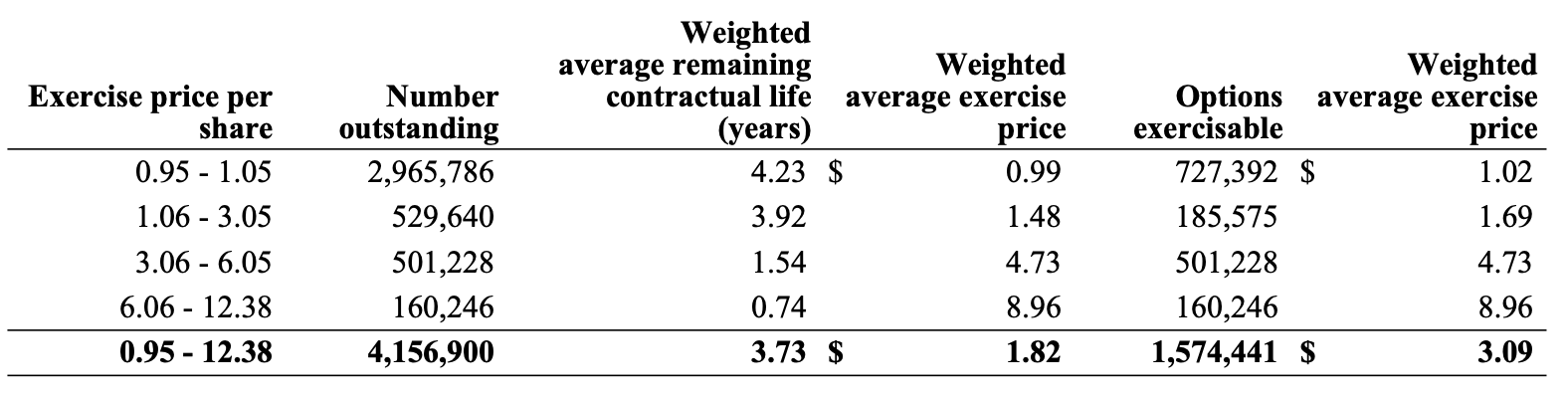

Options outstanding: 4.16 million — average exercise price: $1.82

RSUs (Restricted Share Units): 2.25 million

DSUs (Deferred Share Units): 1.00 million

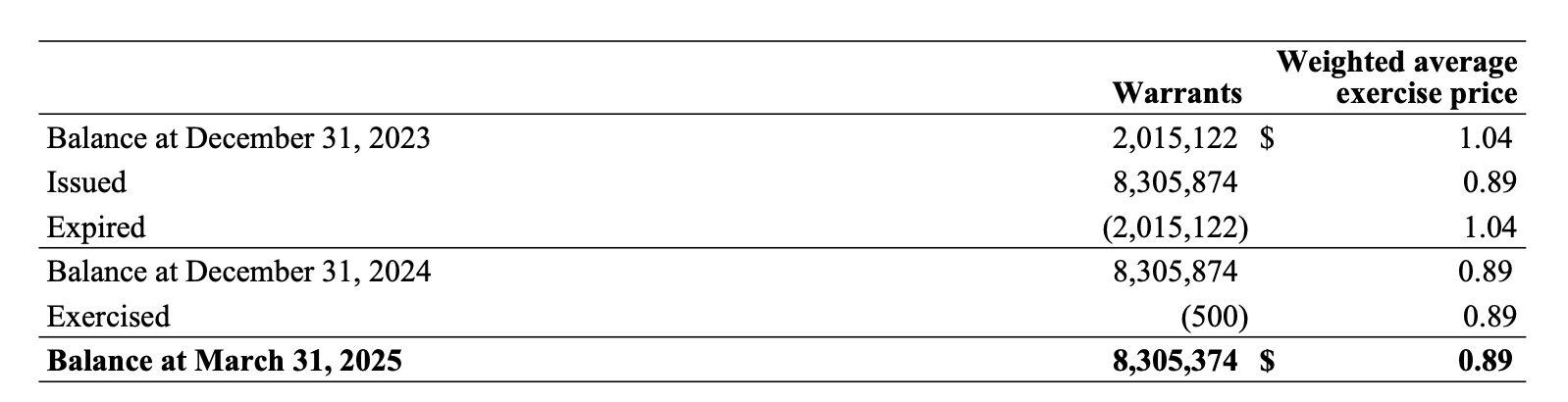

Warrants outstanding: 8.31 million — average exercise price: $0.89

Convertible debt dilution (if fully converted): 13.83 million

Fully diluted shares outstanding: 188.3 million

Financials

Financial Summary (as of March 31, 2025)

Cash & Cash Equivalents: $61.1 million

Restricted Cash: $15.2 million (primarily reclamation-related collateral)

Total Current Assets: $115.0 million

Total Assets: $240.6 million

Debt & Liabilities

Convertible Debt Facility:

Outstanding: $15.0 million

Maturity: July 2027, 9.25% interest

Convertible at $1.22/share with $5M remaining undrawn

Classified as current due to investor convertibility

Derivative liability value: $4.8 million

Total Debt (including equipment loans): $19.1 million

Total Liabilities: $108.8 million, including:

Lease liabilities: $6.6 million

Reclamation liabilities: $56.9 million

Profitability (Q1 2025)

Revenue: $57.0 million (gold & silver sales from Florida Canyon)

Net Income: $0.98 million

Gross Profit: $15.5 million

Operating Cash Flow: $16.1 million

Valuation

As of the time of writing, Integra Resources trades at US$1.60 per share. With 188.3 million fully diluted shares outstanding as of March 31, 2025, this implies a fully diluted market capitalization of approximately US$301 million.

The company reported:

US$61 million in cash and cash equivalents

US$19 million in total debt

This results in an Enterprise Value (EV) of approximately:

EV = Market Cap - Cash + Debt = 301M - 61M + 19M = US$259 million

For each project, I’ll estimate after tax NPV using three gold price environments—$2,500, $3,000, and $3,500/oz—and four discount rates—5%, 8%, 10%, and 12%,

These are very rough estimates based on current assumptions and available data. They reflect my personal view of what seems reasonable as of now but may become inaccurate as new information emerges or company plans evolve.

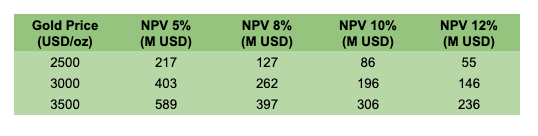

Florida Canyon NPV

Base Case (No Mine Life Extension)

Assumes no material extension beyond the current mine plan (through 2030), with production and costs aligned with recent disclosures.

Assumptions:

Gold production: 70,000 oz/year

Mine life: 2025–2030 (6 years)

Total LOM production: 420,000 oz

AISC: $2,300/oz

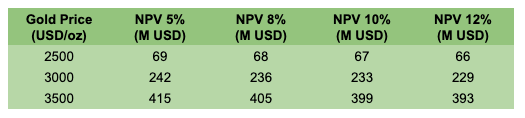

Author Model: After-Tax NPV at Gold Prices from $2,500–$3,500

At $3,000/oz gold and 8% discount rate, this scenario yields an estimated NPV8 of $179 million.

Extended Case (+3 Years)

Assumes successful mine life extension to 2033 through near-mine drilling and resource conversion. This scenario is consistent with recent management commentary suggesting potential for 2–4 additional years.

Assumptions:

Gold production: 70,000 oz/year

Mine life: 2025–2033 (9 years)

Total LOM production: 630,000 oz

AISC: $2,300/oz

Extending the mine life by 3 years increases total gold output by 50%—from 420,000 oz to 630,000 oz—and results in an average ~32% uplift in NPV across gold price and discount rate scenarios. At $3,000/oz gold and an 8% discount rate, the NPV rises from $179M to $236M, a $57M increase—notable when compared to Integra’s current enterprise value of $259M.

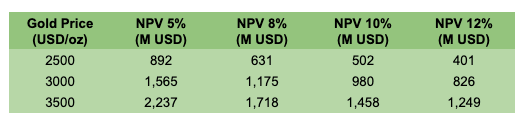

DeLamar NPV

Building reasonable assumptions for Delamar is more challenging, as the company is transitioning from the 2022 PFS to a new Feasibility Study (FS) that focuses exclusively on heap leaching. For more accurate figures, we’ll need to wait for the FS results. That said, here’s my current base case framework:

Construction Start: 2028 — assuming the permitting process (via NEPA) takes at least two more years, as indicated in recent filings.

Construction Timeline: 18 months, consistent with the PFS.

First Full Production Year: 2030 — based on an 18-month construction period following final permit approval.

Production: 110,000 oz of gold and 2 million oz of silver annually — broadly in line with the first 7 years of leach-only production outlined in the PFS.

Source: 2022 PFS Initial Capex: $400 million — up from $307M in the PFS, reflecting inflationary pressures since 2022. While some optimizations may offset part of the increase, I prefer to remain conservative.

AISC: $1,150/oz — higher than the $955/oz AuEq in the PFS, reflecting reduced silver credits and cost inflation, partially offset by the decision to exclude mill construction (originally planned for Year 3) in the current leach-only plan.

Gold-to-silver price ratio: 90:1 — used to convert silver revenue into gold-equivalent ounces for cost and valuation modeling

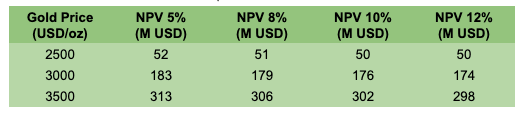

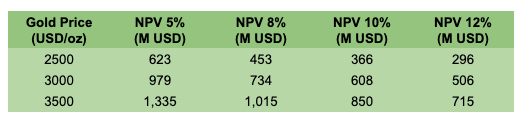

Based on the assumptions above, the base-case after-tax NPV at $3,000/oz gold for DeLamar—discounted at 8% to today—is estimated at approximately $734 million USD.

Nevada North NPV

Valuing Nevada North is even more speculative, given the earlier stage of the project and the fact that only a Preliminary Economic Assessment (PEA) is available. To provide a broad directional estimate, I’ve used a simplified valuation approach based on the PEA. These are conservative assumptions that likely differ materially from eventual project economics:

Assumptions:

First Full Production Year: 2032

Production: 80,000 oz AuEq/year — consistent with the PEA life-of-mine average (LOM was 80k, with ~94k in the first 5 years).

LOM: 10 years — shorter than the PEA’s 13-year mine life, as discounting beyond 2042 has limited relevance; 10 years should suffice for a conservative estimate.

Initial Capex: $300 million — significantly above the $115 million stated in the PEA, reflecting both potential scope expansion and cost inflation.

AISC: $1,300/oz — higher than the $973/oz in the PEA, to account for the early-stage nature of the cost estimates and likely escalation in actual build-out

Based on the assumptions above, the base-case after-tax NPV at $3,000/oz gold for Nevada North—discounted at 8% to today—is estimated at approximately $262 million USD.

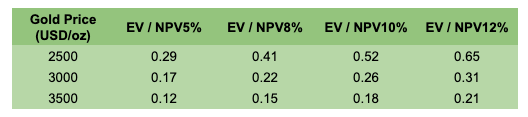

Valuation Summary

Summing up the estimated NPV values across Integra’s three projects, we arrive at a total NPV8% of approximately $1.17 billion and NPV10% of nearly $1.0 billion at a gold price of $3,000/oz. This translates to a current EV/NPV8% multiple of just 0.22 and EV/NPV10% of 0.26, based on an enterprise value of ~$259 million.

In my view, Integra remains significantly undervalued. A more reasonable valuation for junior developer with two assets in development. U.S.-based heap leach production and a permitting-advanced flagship like DeLamar would be in the >0.6× EV/NPV8% range. Over time, as the company progresses DeLamar through permitting and Nevada North toward feasibility—while Florida Canyon continues to generate cash flow—a re-rating toward 1.0× EV/NPV8% would not be unreasonable. That said, it may take a few years to fully realize this revaluation.

Additionally, my sum-of-the-parts model does not ascribe value to Florida Canyon’s potential mine life extension beyond 2030, nor to the broader exploration portfolio (e.g., BlackSheep, War Eagle, and Red Canyon). If even a modest portion of these targets convert into economic resources or satellite feed for existing infrastructure, the company’s NAV could increase —potentially adding another 10–20% upside not reflected in the base-case valuation.

Risks

As a multi-asset developer with one producing mine and two projects at different stages of advancement, Integra Resources carries a range of technical, regulatory, and market risks. Several key risk factors should be considered:

Permitting Risk (DeLamar & Nevada North)

Integra’s flagship DeLamar project is entering the formal NEPA permitting process, which includes public consultation, environmental assessments, and agency reviews. The timeline is expected to span at least two years, but delays are common. Any protracted review or legal challenge could push out the construction decision and increase holding costs. Nevada North will follow a similar regulatory path, compounding overall permitting exposure.

Project Execution and Timeline Slippage

Florida Canyon is undergoing mine optimization, while DeLamar is still in the pre-construction stage. Delays in technical studies, capital raising, or contractor mobilization could defer cash flow generation, negatively impacting valuation and investor confidence.

Gold Price Sensitivity

Florida Canyon operates with relatively high all-in sustaining costs (AISC US$2,342/oz as of Q1 2025). Any material decline in gold prices could quickly erode operating margins and free cash flow, especially as the mine is currently Integra’s only cash-generating asset. To partially mitigate this risk, the company has implemented a downside protection strategy for 2025 by purchasing gold put options—allowing it to retain upside exposure while securing a floor price on a portion of production.

Operational Risk at Florida Canyon

The success of the optimization plan and heap leach upgrades at Florida Canyon is not guaranteed. Failing to reduce costs, maintain recoveries, or extend mine life would reduce the asset’s contribution to corporate cash flow and investor perception.

Execution Complexity Across Projects

Managing permitting, feasibility work, exploration, and operations across three assets increases complexity and potential for missteps.

Milestones

These are the next key milestones I’ll be monitoring closely, as they could significantly influence Integra’s valuation and risk profile:

Florida Canyon

Release of formal 2025 production and cost guidance

Results from 10,000-meter near-pit RC drilling campaign (targeting mine life extension)

Updated resource estimate and revised mine plan (expected in early 2026)

DeLamar Project

Progression to Notice of Intent (NOI) under the NEPA process (targeted by year-end 2025)

Completion of Feasibility Study focused on oxide heap leach development (H2 2025)

Nevada North

Decision Record and Finding of No Significant Impact (FONSI) for Wildcat EA (expected mid-2025)

Results from upcoming metallurgical and geochemical studies

Initial scoping work toward a future PFS or FS

Corporate / Strategic

Insider buying activity (or lack thereof)

Financing strategy for DeLamar (equity, debt, stream)

Conclusions

Integra’s transition from a multi-asset developer to a junior producer with a multi-asset development pipeline marks a pivotal moment. The acquisition of Florida Canyon was, in my view, a strategically important move—it not only adds near-term cash flow but also meaningfully reduces dilution risk as the company advances its larger development portfolio. Having a producing mine in Nevada gives Integra operational credibility and infrastructure that will support the buildout of DeLamar and potentially Nevada North.

With Florida Canyon now generating cash, management has the flexibility to advance key de-risking milestones at DeLamar and Nevada North without needing to raise additional equity—assuming gold prices remain supportive. I also think there’s an underappreciated synergy between the assets: Florida Canyon’s proximity to Nevada North could allow for infrastructure reuse and shared operational expertise, which is increasingly valuable in a tight labor and contractor market.

A major near-term catalyst could come from extending Florida Canyon’s mine life beyond the current six years. The company is actively drilling near-pit oxide targets, and even a 2–3 year extension would meaningfully improve project-level NPV and could support a valuation re-rating.

That said, the lack of significant insider ownership is, for me, a major red flag. I view this as a weak point in the investment thesis—something I’ll be watching closely. I’d like to see recent executive hires begin buying stock in the open market as a signal of long-term confidence in the company.

At current levels, I believe Integra is too cheap to ignore. The stock trades at just ~0.22× EV/NPV8% based on my base-case estimates—a deep discount given the asset quality, jurisdictional profile, and pipeline depth. I’ve initiated a small position and will continue to monitor permitting progress, feasibility work, and insider activity. I don’t feel comfortable taking a full position yet until I see more “skin in the game” from management and the board. If the company executes well and alignment improves, I plan to increase my position—assuming the valuation still looks compelling.

Thanks for taking the time to read my deep dive—I hope you found it helpful.

I’d really appreciate your feedback in the comments:

What did you find most useful?

Which sections felt too light or too detailed?

Are there areas you’d like me to explore more thoroughly in future write-ups?

I’ll try to improve with each new piece.

Also, if there are specific companies you’d like me to cover next—especially in the gold, silver or uranium — drop them below. I’m always looking for new ideas worth digging into.

Thanks again for your time.

Want to support the next edition? A coffee would mean a lot and help me keep digging

Nice summary. Rio2 and Integra are two of my largest positions in the gold space so good to see I'm not the only one. Rio2 is a mintwit darling but Integra is very much the opposite. For Integra, I think people are clouded by past judgments and bias against the company (and its management team). Yeah it wasn't worth 10-12 CAD a few years ago but it's definitely worth more than the current share price at the current gold price. The risk/reward at this price is completely asymmetric.

Management kind of lucked out with FC and the gold price increase but it is what it is, and that will tick a long nicely and provide cash-flow to develop Delamar and Nevada North which will be better operations than FC. My assumptions / valuations are probably slighter different than yours. I've got:

Florida Canyon (Including 3 Year Extension): ~$300m (USD) @2,750 Gold

DeLamar (Currently): ~$200m (USD), implies ~0.2x of PFS NPV (with some adjustments) or ~$60 per Oz of Resource

Nevada North (Currently): ~$100m (USD), implies ~0.2x of PEA NPV (with some adjustments) or ~$60 per Oz of Resource

So I'm looking at ~600m USD or about $5 CAD over next 18 months. If Delamar develops faster then probably deserves an uptick.